{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

I am just back from our Annual Convention and I’m still buzzing from the good vibes, great education and amazing connections I made while there. As I’ve previously talked about, the mid-year is a great meeting for connecting on an intimate level and invaluable as a first-timers conference, but nothing quite matches the vibrant atmosphere of our Annual Convention, and this year was truly exceptional. We were thrilled to welcome pre-pandemic attendance numbers, showcasing the resilience and enthusiasm of our community.

I am just back from our Annual Convention and I’m still buzzing from the good vibes, great education and amazing connections I made while there. As I’ve previously talked about, the mid-year is a great meeting for connecting on an intimate level and invaluable as a first-timers conference, but nothing quite matches the vibrant atmosphere of our Annual Convention, and this year was truly exceptional. We were thrilled to welcome pre-pandemic attendance numbers, showcasing the resilience and enthusiasm of our community.

The Convention and Education Committees deserve immense praise for curating an outstanding program that catered to diverse interests and needs. From special events and education tailored to our emerging leaders to dedicated sessions and networking opportunities for our international members, there was something enriching for everyone. I am especially delighted to note that we welcomed 20 new attendees to our meeting this year, demonstrating the growing interest and relevance of our community.

This year, we decided to shake things up by adjusting the schedule. Rather than starting on Wednesday night with the Welcome Celebration, we began with afternoon education on Wednesday followed by our cocktail parties and Welcome Celebration. We also moved our special event (typically on Thursday night) to a luncheon on Thursday. We had amazing food and a fun atmosphere at Nikki Beach, which got us outside and enjoying each other’s company in a more casual setting.

The mid-afternoon wrap-up on Thursday allowed attendees to savor quality time with loved ones, explore the area, or simply relax on the beach—an experience that was warmly received by many. It also allowed everyone to plan for dinner on their own, which was a departure from our past conventions. The people we’ve heard from so far have loved it— but we want to hear from you! If you loved it or hated it, please let us know. Especially because we’re planning this new schedule for next year’s Annual Convention in Puerto Rico!

Education Round Up

One of the highlights of the convention was undoubtedly our keynote address, “AI… Be a Friend or Be Afraid.” Talk about timely! Tom Morrison captivated us with insights into how AI can streamline processes, enhance decision-making, and revolutionize customer interactions, as well as giving us quite a few takeaways from the session.

We had an array of activities focused on international education and networking. These provided valuable opportunities for our members to delve into the nuances of cross-cultural communication and the challenges of global compliance. We engaged in interactive discussions, sharing experiences and strategies to navigate the complex international landscape.

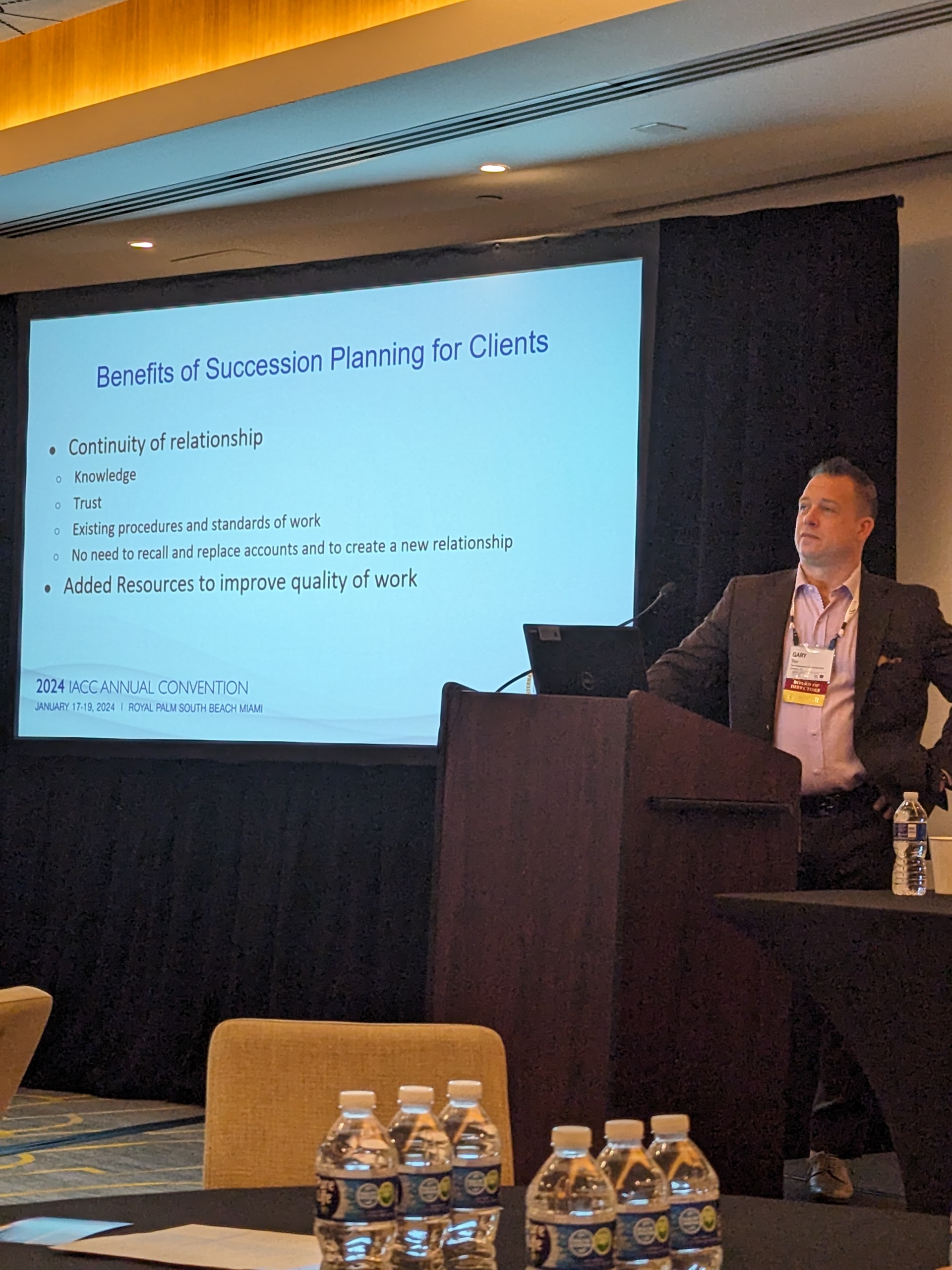

A special segment of the convention was dedicated to emerging leaders in the collections field. Seasoned professionals and new entrants alike benefited from the emerging leaders’ session, “Succession Planning and Strategic Mentoring,” fostering a sense of community and collaboration that is essential in today’s globalized world.

We also had the privilege of gaining insights from Ghandi Eswaramoorthy of the Consumer Financial Protection Bureau (CFPB). With a wealth of expertise in consumer finance and regulatory compliance, he offered invaluable guidance on navigating the evolving landscape of the collections industry. Through his presentation and interactive discussion, we had the opportunity to deepen our understanding of regulatory requirements and explore proactive approaches to address emerging challenges.

Networking and Recognition

Beyond the formal sessions, the conference overflowed with opportunities for networking. From breakfasts to coffee breaks to fun evening social events, attendees formed connections that promise to extend well beyond the event. These informal gatherings were not only a highlight for many of us, but also a testament to the vibrant and collaborative spirit of the IACC community.

Finally, I extend my heartfelt congratulations to this year’s award winners: Rebecca Robitaille (Associate) and Michelle Lindsay (Agency) for the Robert P. Ingold Emerging Leader Award, and Jim McConville for the IACC Leadership and Distinguished Service Award. Your contributions are truly commendable!

Looking Ahead

It’s clear that the collections industry is at a pivotal juncture. The integration of AI and a strong focus on global initiatives are not just trends, but have the ability to reshape the core of our profession, propelling us toward a future where innovation and learning will go hand in hand to meet the evolving needs of our industry.

We thank all our esteemed speakers, panelists, and attendees for making the IACC Convention a resounding success. Let’s continue to innovate, inspire, and lead as we eagerly anticipate next year’s conference in Puerto Rico!

Speaker: Colin Winkler Senior Counsel, ACA International

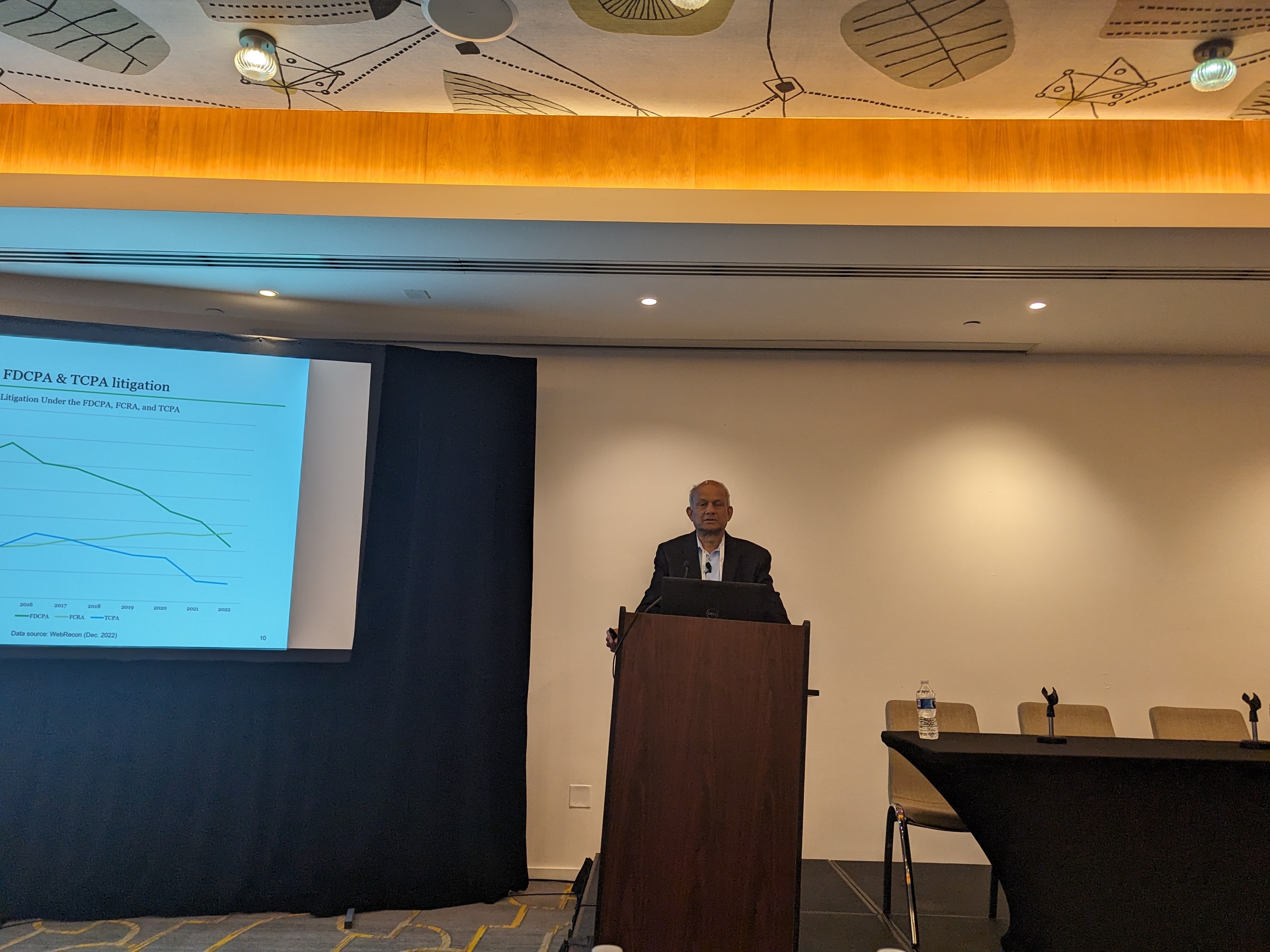

Colin Winkler, ACA International’s senior counsel, gave a legal update on commercial debt collection during the IACC Annual Conference, discussing recent actions from the Consumer Financial Protection Bureau and other regulators, as well as trends in business practices. Here are some highlights from his presentation on coming changes to the industry.

The CFPB Winkler said the CFPB has been very active in the consumer space, but commercial collection has remained relatively calm. In 2022, Rep. Al Lawson, D-Fla., introduced legislation to expand the Fair Debt Collection Practices Act to cover commercial collections, but that bill died in committee. “To my knowledge, we have not seen an attempt from Rep. Lawson or anyone else to resurrect it,” Winkler said. The CFPB remains very interested in demographic disparities in the small business segment.

One example of that is the CFPB’s Small Business Lending Rule, which requires lenders to disclose credit applications they receive from small businesses, lending decisions and demographic data. The resolution passed in the U.S. Senate but was voted down in the House and vetoed by President Biden in December 2023. The Senate then approved a joint resolution to override that veto, but could not muster enough votes.

“We don’t often see Congressional Review Act action on a federal rule like this,” Winkler said. “And again, because the Senate could not muster the votes to override the veto, the rule did take effect, but it remains on hold—at least as a practical matter—as a result of a couple of federal injunctions pending the SCOTUS decision in Consumer Financial Services of America v. CFPB. Federal courts in Kentucky and Texas issued injunctions that for now prevent the CFPB from enforcing this rule. Those cases rest primarily on the argument that the CFPB lacks a constitutionally appropriated funding mechanism. And that’s the argument that the Supreme Court heard in October 2023 in CFSA v. CFPB.”

A decision in that case is expected by the end of June 2024.

“That will go a long way toward determining whether and how the CFPB can take action,” Winkler said. “I think most court watchers expect that the Supreme Court is going to say the CFPB does have a constitutional funding mechanism, but that is just based on speculation of court watchers from around the web.”

Winkler said these events are important for IACC members to know about because they are indicative of the CFPB’s mindset, which might impact conversations you have with your clients.

The FTC The Federal Trade Commission enforces commercial collections violations. The enforcement cases it has pursued recently have been for egregious violations, like in FTC v. RCG Advances LLC, where the commission sued the company and its owners for unfair commercial debt collection practices when collecting on merchant cash advances, including sometimes threatening physical violence.

And in a 2022 case, the FTC said Yellowstone Capital, which was a provider of merchant cash advances, continued withdrawing money from businesses’ bank accounts after their balance had been repaid. The FTC initiated an enforcement action that resulted in nearly $10 million dollars being returned to those businesses.

“If the FTC is focusing on behavior like this, then I think from a federal regulatory perspective, the commercial collection space is in pretty good shape,” Winkler said. “Still, it remains to be seen what’s on the horizon for commercial collections in 2024 as they continue to advance their fairly aggressive agenda.”

The TCPA Determining whether a phone number is a business or residential line for Telephone Collection Practices Act purposes has become more complex, so proper consent is important.

The FCC’s “lead generator rule” requires one-to-one consent for calls related to leads, which could impact how consent is obtained and applied.

“The whole TCPA landscape has gotten significantly muddier for what I think of as business-to-business collections calls because of the integrated technology we have now, where a cellphone can have a dual purpose as a business line and also exist—in at least a court’s and the FCC’s mind—as a residential telephone line,” Winkler said. “And then again, that one-to-one consent rule muddies the waters. Some of us may have been relying on consent obtained through a lead generator, but now that’s got to be obtained on a one-to-one basis.”

Also, IACC members should keep in mind that their calls to cellphones may be blocked or mislabeled as spam. Be ready to work with your carriers through the FCC’s robocall mitigation database to address any mislabeled calls.

Personal Guarantors

Pursuing personal guarantors of commercial debts could potentially lead to FDCPA liability if not handled carefully.

“I think you need to understand how sophisticated your clients’ clients are,” Winkler said. “A lot of people who sign a personal guarantee don’t know what it is exactly they’re signing for their small business. A lot of those consumers won’t understand that you’re collecting a business debt, and that they’re not entitled to the protections of the FDCPA. And by attempting to enforce that personal guarantee, you could be creating risk for yourself. So again, I think that’s the kind of risk assessment you have to do by understanding your clients’ portfolio and who it is you’re ultimately going to be calling. Because often the small businesses are going to be defunct by the time you end up going to collect and it will be the individual guarantors you’re collecting from.”

Winkler said he does see cases like that in bankruptcy courts and in federal district courts. He said he generally sees courts asking, “What’s the [essence] of this agreement? What was it for and for what was it used?”

“And if it’s for business purposes, then you’re good,” Winkler said. “But as we just talked about, regardless of a personal guarantee, if that loan or equipment or vehicle ended up being used for personal or household purposes, that’s what the courts tend to look at under the FDCPA.”

An attorney in the audience said that her company started including a sentence in their demand letters that says: “You are receiving this letter because you have personally guaranteed a commercial debt.’”

Electronic Consent

Winkler said he is seeing more court cases on electronic consent, which has to do with understanding what sort of an agreement your client has secured from their client.

Electronic consent generally comes in two flavors: browsewrap and clickwrap.

Browsewrap assumes users have accepted an agreement if they use the website.

For example, the website might say: “If you submit this form, you’re agreeing to our Terms and Conditions.” The terms are usually hyperlinked, but the consumer doesn’t necessarily have to look at those terms and conditions in order to advance through the process of getting whatever it is they need. This matters because it affects contract formation, Winkler said.

Most lawyers and judges prefer clickwrap, which forces consumers to demonstrate assent to terms and conditions by having them check a box that indicates their consent.

“We’ve seen, particularly out of the 9th Circuit, a number of cases that have found that while browsewrap can be enforceable, it really needs to be prominent,” Winkler said. “And when we say that in the browsewrap context the terms and conditions need to be conspicuous, we’re talking at least as large, if not larger than, the surrounding font, a different color, ideally bold faced, and ideally with surrounding text that calls attention to them with a line break. You want something that a judge is going to look at and say, ‘There’s no way that whoever is being held to the agreement could have missed this.’”

This year’s award winners were recognized for their dedication and commitment to the betterment of IACC and the commercial collection industry. In addition to being recognized in this month’s issue of Scope, these award recipients were recognized at IACC’s 2024 Annual Convention in January.

IACC 2024 Robert P. Ingold Emerging Leader Award

This award recognizes early-careerminded collection agency (or law firm) professionals who have completed notable work of merit within their organization and IACC, and have demonstrated significant promise of leadership, service and professionalism within the collection services industry.

This year’s Agency Emerging Leader is Michelle Lindsay of ABC-Amega, Inc. Lindsay was brough to her first IACC convention last year and has hit the ground running by joining committees and being involved in the growth of the association. She has shown strong leadership skills not only within her organization but within IACC as well.

As part of her role as award winner, she will be serving as the chair of IACC’s Emerging Leaders Committee this year and holds a non-voting, honorary seat. *This award winner becomes the new Honorary Board Member for the Emerging Leader program as of the January board meeting.

This year’s Associate Emerging Leader is Rebecca Robitaille of Franklin & O’Brien Legal Services Inc. Robitaille joined IACC’s Emerging Leaders and Communications committees, and her voice is helping to shape the future of the IACC as well as how the IACC is presented to the membership and beyond.

This year’s Associate Emerging Leader is Rebecca Robitaille of Franklin & O’Brien Legal Services Inc. Robitaille joined IACC’s Emerging Leaders and Communications committees, and her voice is helping to shape the future of the IACC as well as how the IACC is presented to the membership and beyond.

IACC 2024 Leadership and Distinguished Service Award

This award is presented annually to an IACC member who has given his or her time and energy to better the association, exemplifies IACC values and standards, has emerged as a leader in our organization and has conducted his or her professional and personal life in a manner that positively impacts the commercial collection industry.

This year’s winner is Jim McConville of Radius Global Solutions, LLC.

This year’s winner is Jim McConville of Radius Global Solutions, LLC.

McConville was nominated for his tremendous, selfless and thoughtful contributions as well as his unwavering enthusiasm to step up and support the IACC. His nominator Greg Cohen had the following to say about Jim: “He is a deep thinker and great communicator. His guidance was spot on during difficult times and tough decisions. We have, thanks to his instincts and calm approach, mitigated any hardship.” He has served on the IACC Board since 2018 and has served as treasurer since 2019.

![]()

Caine & Weiner, an IACC member company with a nearly 100-year history, announced a strategic shift in its executive leadership structure recently. Greg Cohen has assumed the role of chairman and chief executive officer, and Joe Batie was promoted to president and chief commercial officer.

Greg served as president since 1999 and president & CEO of Caine & Weiner since 2008. During his tenure, he led the company through significant growth and transformation, expanding its product offerings, strengthening its leadership team and customer base, and enhancing its financial performance.

Greg will focus on the company’s long-term strategic direction, ensuring its continued success in the evolving financial services landscape. Joe Batie, having served as Caine & Weiner’s chief commercial officer for the past 10 years, brings over 37 years of experience in the financial services industry to his new role as president and CCO. He has a proven track record of success in driving revenue growth, expanding market share, and building strong customer and alliance partner relationships.

In his new role, Joe is responsible for the company’s day-to-day operations, overseeing all aspects of its business, including operations, sales, marketing, product development, and customer service.

“I am excited to announce this strategic transition in our executive leadership,” Cohen said. “Joe is vastly experienced, a trusted and respected leader, well-rounded and deeply invested in all aspects of our stakeholder’s success.

“Joe, along with our outstanding leadership team, have significantly contributed to our company’s longstanding commitment to provide best-in-class Receivable to Cash Solutions and our succession roadmap which has been at the core of our commitment for over 93 years.

I will remain fully engaged post this transition confident that he will continue to lead our team with the same dedication, vision and expertise that have characterized his career.”

Batie added, “I am honored to be promoted to president and chief commercial officer of Caine & Weiner. I am deeply committed to the company’s mission of providing exceptional financial services to our customers. I look forward to working with our talented team to achieve continued growth and success.”